Last Updated on June 23, 2026

One of the secrets to managing your finances is to abide by credit card best practices. If you follow these rules for credit card use, you’ll be able to stay in control of your family’s finances.

Responsible use of credit cards is a great way to strengthen your credit score. And there’s no denying the convenience of paying with credit since it allows us to shop online (which can help us save money!) and eliminates the need to carry around a large amount of cash. In order to enjoy the benefits of credit cards without falling into a debt trap, follow these credit card best practices.

Credit Card Best Practices

1. If you can’t afford it now, you probably can’t afford it later. Don’t use your credit card as a portable lender. It’s a tool to build your credit score, earn perks, and make shopping more convenient. It shouldn’t be a way to get things you don’t have the money for.

2. Pay your bill on time or early every month. Late fees are steep and make that 20% discount you scored in the first place obsolete. Also, the interest rates kick in once your payment is late. Late payments ruin your credit score as well, making it difficult to get loans for things you really need a car or a home.

3. Don’t get a new card every time a clerk suggests it. Sure, you may get a discount. But what if it encourages you to just buy more next time? More purchases equal more spent money equals more credit card debt. Just say no.

4. Avoid gimmicks. Those incentives that credit card companies offer sure are enticing! Don’t spend your money to earn the “free” perks. Instead, choose credit cards that offer perks you know you will have a use for (e.g. airline miles if you travel a lot) and then let the points or miles accrue naturally as a result of your regular shopping. Treat them as your reward for choosing one credit card company over another, not as goals you have to meet.

5. Keep a low-to-no-balance. The idea of a credit card is that it’s there when you need it. Like when you’re in the middle of the Mojave desert and there’s not an ATM in sight. Or when you’ve got a sleeping toddler in the backseat and you need to fill up with gas. Wanting a whole new wardrobe because last year’s clothes are out of style is NOT a need, especially when you can only afford a new pair of pants.

6. Don’t use an easy pin. I know you want your pin to be easy for you to remember, but that doesn’t mean it has to be easy for someone else to guess. Is your pin 1111? 1234? 6969? If so, change it. These are three of the most common pins people use and they’re the first codes thieves will try if they get a hold of your card. Stick with birthdays, addresses, or some other personal number that is easy for you to remember, but difficult for a stranger to guess.

7. Don’t leave your credit card information around. Never include the Card Security Code (CSC), the expiration date or the full number on checks for payment. If you keep copies of your credit card information, be sure to keep it in a secure location.

8. Don’t respond to inquiries from credit card companies that you didn’t initiate. There are a lot of identity thieves, fishing scams and credit card scams around. If you get an e-mail from someone claiming to be your credit card company, do not click on the link within the e-mail. Instead, type your credit card company’s URL into your browser address bar and log into your account to see if you have any messages there. If someone calls claiming to work for your credit card company about a problem with your account, hang up and call the customer service number on the back of your card.

9. DO leave a copy of the front and back of each card behind, perhaps with a trusted friend or loved one, when you go on vacation, and bring the helpline phone numbers with you. In the event of loss or theft, you’ll know who to contact and what the numbers were.

10. Be responsible. Ultimately, all of these tips boil down to putting on your grown-up pants and acting responsibly. Use your card judiciously, pay off balances as soon as possible, pay on time, and be discreet with your card.

Would you like to save this?

More Financial Resources

If you struggle with spending responsibly, I promise that the book The Recovering Spender by Lauren Greutman can help. Lauren and her husband climbed their way out of over $40,000 in debt. To learn more about Lauren and the book, you can read my review or you can purchase the book immediately on Amazon.

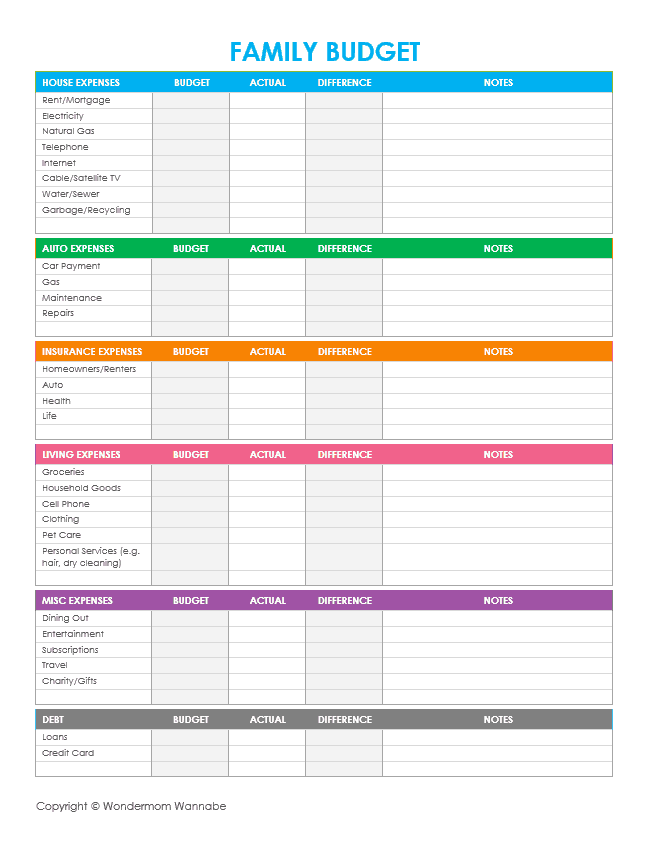

Another way to stay on top of your finances is to create a budget and track your spending. I’ve created some free budget worksheets to help you do that.

If spending isn’t your problem and you just want some tips for planning your savings, read my Tips for Creating a Family Savings Plan.